The $700 Billion Short

While Finans Obsesses Over a Romanian CEO, Wall Street Is Buying Denmark With Denmark's Own Money

Prologue: Two Headlines

On the morning of February 4, 2026, two things happened in Denmark.

The first: Novo Nordisk—the company that represents nearly half of Denmark’s entire stock market capitalization—lost seventeen percent of its value in a single session. Fifty billion dollars. Gone. The largest single-day destruction of Danish wealth in modern history.

The second: Finans, Denmark’s premier business publication, published another article about Shape Robotics.

If you want to understand why Denmark is dying, you don’t need economic theory. You don’t need policy papers. You just need to sit with those two facts for a moment and feel the weight of what they reveal.

A country watching its crown jewel collapse.

A media obsessed with a Romanian CEO.

This is the x-ray of a nation that has stopped thinking.

Part I: The Day the Music Stopped

Copenhagen, 9:00 AM, February 4, 2026

Lars Andersen—let’s call him Lars—has managed pension money for seventeen years. He’s good at his job. Cautious. Danish. He believes in systems.

At 9:00 AM, his Bloomberg terminal turned red in a way he’d never seen.

Novo Nordisk was down eight percent. Then ten. Then fifteen. By lunch, it would settle around seventeen percent—a $50 billion evaporation.

Lars did what Danish professionals do: he called his colleagues. They called their colleagues. Everyone asked the same question: What happened?

Here’s what happened: Novo announced that sales and operating profit would decline 5-13% in 2026. Pricing pressure in America. Competition from Eli Lilly. The Wegovy dream was hitting reality.

But that’s not what really happened.

What really happened is that someone knew this was coming.

The Positioning

In the summer of 2025, while Danish journalists were writing puff pieces about sustainability and green transitions, something unusual was happening in Chicago, New York, and London.

Citadel Advisors was accumulating put options on Novo Nordisk.

So was Susquehanna.

So was Jane Street.

So was Barclays.

So was D.E. Shaw.

A put option, for those unfamiliar, is a bet that a stock will fall. When hedge funds buy puts at scale, they’re not hedging. They’re hunting.

The question Lars should have asked—the question every Danish pension manager should have asked—is: What did they know that we didn’t?

The answer is simple: they were willing to think. Denmark wasn’t.

Part II: The Distraction

What Finans Published That Morning

While Novo was collapsing, I checked Finans.dk.

The front page featured another story about Shape Robotics.

Let me make sure you understand the proportions here:

Novo Nordisk: $50 billion destroyed in one day.

Shape Robotics: A company with DKK 325 million in revenue—about $45 million.

The ratio of destruction to coverage was approximately 1,000 to 1 in the wrong direction.

This is not journalism. This is obsession. And obsession always tells you more about the obsessed than the object.

Why Finans Can’t Stop Writing About Me

I’ll tell you why, because I’ve had eighteen months to study the pattern.

In December 2025, Finans sent me an email. They had “another story coming up” about my former role at Sav Integrated Systems—a Romanian company I was a minority shareholder in, not the CEO, not the chairman.

They had quotes from two “experts”—law professors positioned as neutral authorities—offering opinions on whether Shape Robotics should have disclosed Romanian legal proceedings that had nothing to do with Shape’s operations.

Here’s what they didn’t disclose:

The Shape Robotics board knew about the Romanian cases when they hired me. They hired a private investigator. They obtained legal opinions. They concluded—correctly—that pending proceedings in another country, involving a different company, with no conviction, did not constitute inside information under MAR.

But that’s not a story. “Board Does Due Diligence, Follows Legal Advice” doesn’t get clicks.

You know what gets clicks? “Romanian CEO.” “Corruption.” “Luxury Cars and Bags of Money.”

The headline they ran translated to exactly that.

I’m Romanian. My name is Mark Abraham. In Denmark, that combination is enough to make me permanently suspicious.

This is how a small country with a superiority complex processes foreigners who don’t know their place: they investigate you until something sticks, and when nothing sticks, they investigate harder.

The Real Function of the Coverage

Here’s the part they don’t teach in journalism school:

When you write relentlessly about a small company during a liquidity crisis, you become part of the crisis.

Every Finans article created a news event. Every news event triggered calls from nervous creditors. Every nervous creditor tightened terms. Every tightened term increased pressure.

Then, when the company struggled under the pressure the coverage helped create, Finans wrote about the struggle—citing the coverage as evidence that something was wrong.

This is not reporting. This is a feedback loop.

I filed a complaint with Nasdaq Copenhagen alleging market manipulation. The complaint documented how a prominent Danish analyst—who held Shape shares—published bullish research, then sold into the rally he helped create.

Forty days later, I was bankrupt.

Coincidence, I’m sure.

Part III: The Parallel Autopsy

Denmark’s Hidden Collapse

While Finans was writing about me, here’s what was happening to Denmark:

The Copenhagen Index: Down 46% from its June 2024 peak.

Novo Nordisk: Down 50% in 2025—its worst year on record.

First North: The growth company exchange lost 57% since 2021. Forty-one companies destroyed.

EIFO: The state export fund fired 50 employees, cut activity to its lowest since 2020.

The tax system: Still taxing unrealized gains on listed shares, driving capital to Sweden.

The bankruptcy system: Still imposing three-year management bans for failure, treating entrepreneurs like criminals.

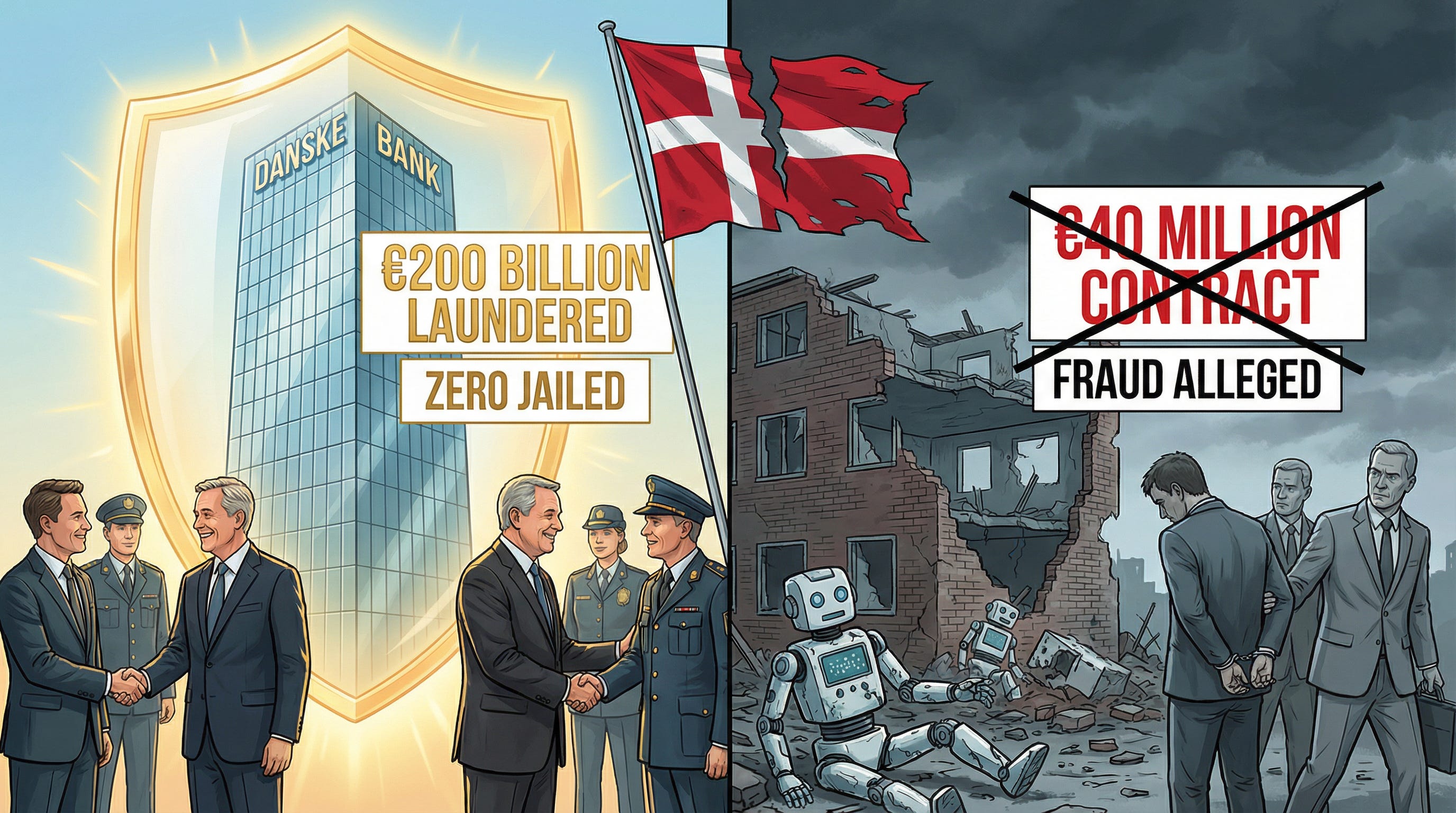

Danske Bank: Still operating normally, despite laundering €200 billion through Estonia. Zero executives jailed.

But sure, let’s write another article about the Romanian.

The EIFO Withdrawal

Here’s a fact that should have been front-page news:

In June 2024, EIFO—Denmark’s export and investment fund—withdrew support from Shape Robotics. The reason? We had graduated from First North to the Nasdaq Copenhagen Main Market.

Read that again.

A company successfully uplisted—increasing its disclosure requirements, its governance standards, its transparency—and the Danish state responded by withdrawing support.

The official explanation: EIFO focuses on unlisted and pre-IPO companies.

The real explanation: Denmark doesn’t have a template for “company that succeeds and grows.” The template is “company that stays small and compliant.” When you break the template, the system rejects you.

EIFO’s withdrawal triggered everything that followed. Credit facilities terminated. Liquidity constrained. Vulnerability increased. And when Finans came calling with their destruction campaign, we had no cushion left.

This is how Denmark kills innovation: not with malice, but with checkboxes.

Part IV: The Sanako Destruction

A €40 Million Contract, Burned

Let me tell you about what happened yesterday.

Shape Robotics had a Finnish subsidiary called Sanako. Sanako held a contract worth €32-40 million to deliver educational robotics laboratories to Polish schools. The project was EU-funded. The financing was in place: €4 million from Alisa Bank and Veritas, guaranteed by Finnvera—the Finnish state.

Sixteen thousand robots. Ready for deployment.

Yesterday, the Danish bankruptcy administrator declared Sanako insolvent.

Forty million euros. Gone.

But here’s the part that made me write this article:

The administrator is now telling journalists that the financing was “credit fraud.”

What “Credit Fraud” Actually Means

Let me explain what contract financing is, because apparently Danish administrators don’t know.

When you have a €32 million contract with a government-backed buyer, and you need €4 million to execute it, you go to a bank. The bank provides the €4 million. You execute the contract. The buyer pays. You repay the bank.

This is called “trade finance.” It’s how international commerce has worked for centuries. It’s how every major infrastructure project gets built. It’s how education technology reaches schools.

We disclosed this financing publicly. Company Announcement 25-25. Company Announcement 28-25. The purpose was stated. The banks knew. Finnvera knew. Every investor who could read knew.

Calling this “credit fraud” is like calling a mortgage “bank robbery.”

But here’s why the administrator is doing it:

He destroyed €40 million of value. He needs someone to blame.

I’m Romanian. I’m available.

The “Cooperation” Farce

The administrator accuses me of “non-cooperation.”

Here’s what actually happened:

They demanded I “cooperate”—without sending me the documents that empower them.

My lawyer formally requested the bankruptcy order and empowerment documents.

They never provided them.

I requested translated documents—I’m Romanian, I’m entitled to understand what I’m signing.

Their response: “Not acceptable. We summon you to court.”

Under EU law, they’re required to provide translations.

You cannot demand cooperation while hiding the documents.

But in Denmark, process is performance. The appearance of propriety matters more than the substance. They can say “he didn’t cooperate” to journalists, and journalists will print it, because journalists don’t read EU regulations.

They read press releases from administrators who need cover.

Part V: The Moral Economy

Ayn Rand Was Right About One Thing

I’ve been thinking about Rand lately. Not her politics—her observation.

She described “looters”: people who produce nothing but grow rich by feeding on those who do. People who use systems, regulations, and moral positioning to extract value from builders.

I used to think this was an exaggeration. A libertarian fantasy.

Then I watched it happen.

The hedge funds didn’t build Novo Nordisk. They shorted it.

The administrator didn’t build Sanako. He liquidated it.

The journalists didn’t build Shape Robotics. They wrote about its destruction.

EIFO didn’t build our export business. They withdrew support when we succeeded.

Danske Bank didn’t create €200 billion. They laundered it.

None of these people built anything. But all of them will survive this. All of them will have jobs next year. All of them will speak at conferences about “responsible governance” and “sustainable business.”

The people who built things—the engineers, the teachers, the Polish schools waiting for robots—they lose.

That’s the moral economy of Denmark in 2026.

The Two-Track System

In December 2025, I wrote about Jeppe Frandsen—the former chairman of Shape Robotics.

Jeppe was also chairman of Paralenz when it went bankrupt in 2022. EIFO lost 25 million DKK on that one. Danske Bank recovered zero.

When Paralenz collapsed, nobody wrote headlines about Jeppe. Nobody questioned his judgment. Nobody suggested he was unfit for leadership.

Eighteen months later, he was chairman of Shape Robotics. Same structure. EIFO guarantee. Danske Bank facility. Same pattern.

And when it collapsed again, nobody asked: “Why did Denmark’s institutions trust this structure twice?”

Because Jeppe is Danish. He knows people. He speaks the language—not just Danish, but Danish: the unspoken codes, the relationship signals, the way you acknowledge mistakes without actually acknowledging them.

I’m Romanian. I document everything. I write things down. I publish my responses to journalists.

In Denmark, that’s not resilience. That’s aggression.

Denmark operates a two-track system: public acceptance and private mistrust coexist until they suddenly don’t. And when they stop coexisting, there’s no conversation about why. There’s just destruction and everyone pretending they couldn’t have seen it coming.

Part VI: The Greenland Trade

What This Is Really About

Now let me tell you why this matters beyond Denmark.

Trump wants Greenland. The reported price: $700 billion.

In January 2026, Trump threatened 10-25% tariffs on Denmark unless there was progress on “complete and total takeover” of Greenland.

The day after the threats, the C25 dropped 2.7%—the worst single-day decline in six months.

Denmark thinks this is about sovereignty. About dignity. About alliance politics.

It’s not.

It’s about leverage.

The Arithmetic of Extraction

If you want to buy something and the seller doesn’t want to sell, you have two options:

Offer more money.

Make the seller desperate.

The second option is cheaper.

How do you make Denmark desperate?

You destroy its optionality. You crash its markets. You turn its national champion—Novo Nordisk—from a point of pride into a point of vulnerability.

And if you’re really sophisticated, you don’t just crash the markets. You profit from crashing them.

The hedge fund short positions are public. Citadel. Susquehanna. Barclays. They’re all in the filings.

The crash is public. Fifty billion dollars on February 4 alone.

The Greenland demand is public. Seven hundred billion dollars.

Connect the dots:

Short Denmark → Crash the market → Profit billions → Use profits to buy Greenland.

I’m not saying this is a conspiracy. I’m saying it’s arbitrage.

The money to buy Greenland may come from destroying Denmark’s own economy.

And Denmark is too busy writing articles about me to notice.

Part VII: The Pattern

What Shape Robotics Revealed

My company was small. In the grand scheme of things, €40 million is a rounding error against Novo’s $50 billion.

But the pattern is the same:

EIFO withdrew support based on a technicality. Not analysis. A checkbox.

Banks terminated facilities during negotiations. Not because the business failed. Because the guarantee disappeared.

Media amplified the crisis. Every article became a news event. Every news event triggered creditor anxiety.

Administrators prioritized procedure over value. Liquidation is safe. Preservation requires judgment. Denmark doesn’t do judgment.

When value was destroyed, blame was assigned. Not to the institutions that failed. To the foreigner who built.

This pattern isn’t unique to Shape Robotics.

It’s the Danish operating system.

And it will destroy Denmark.

The Innovation Graveyard

First North has lost 57% of its value since 2021.

Forty-one companies gone.

Orbex—the rocket company. Bankrupt.

Aquaporin—Nobel Prize-winning water technology. Bankrupt.

Shape Robotics—educational technology deployed across Europe. Bankrupt.

These weren’t frauds. These weren’t failures of entrepreneurship. These were companies killed by a system that punishes success, withdraws support on technicalities, taxes unrealized gains, and treats bankruptcy as moral failure.

In Silicon Valley, failed founders are preferred by investors. They’ve learned something.

In Denmark, failed founders are quarantined. Banned from management for three years. Marked forever.

The message is clear: don’t try. And if you try, don’t fail. And if you fail, don’t expect to try again.

This is how a society commits economic suicide while lecturing the world about sustainability.

Part VIII: The Choice

What Denmark Can Do

Denmark has one asset left that the world wants: Greenland.

Two million square kilometers. Rare earth minerals. Strategic Arctic position. Potentially the most valuable real estate of the 21st century.

Trump is offering $700 billion.

Denmark can either:

Option 1: Fix itself.

Reform the tax system (stop taxing unrealized gains).

Reform EIFO (support companies that succeed, not just pre-IPO).

Reform bankruptcy law (failure is tuition, not crime).

Reform the media (demand disclosure of financial interests).

Prosecute actual crime (€200 billion in money laundering, not €40 million in contract financing).

Option 2: Sell Greenland.

Because a country that cannot preserve a €32 million contract inside its insolvency system has no business believing it can out-negotiate a superpower.

Markets price incompetence in real time.

Right now, Denmark’s price is falling.

What I’m Going to Do

I’m going to document everything.

Every withdrawal. Every termination. Every accusation. Every procedural failure.

I’m going to publish it—not for revenge, but for the record.

Because somewhere in Europe, there’s another founder considering Denmark. Another investor evaluating Copenhagen. Another company thinking about expansion.

They deserve to know what they’re walking into.

They deserve to know that in Denmark:

Success triggers withdrawal of state support.

Graduation is treated as disqualification.

Media writes about foreigners until something sticks.

Administrators destroy value and allege fraud to cover it.

Banks launder €200 billion and face no consequences.

Entrepreneurs build companies and face three-year quarantines.

This is Denmark 2026.

And this is also why Denmark is dying.

Epilogue: The Red Screen

Lars the pension manager is still staring at his screen.

He’s lost count of how many billion kroner evaporated today. His fund is down. His colleagues are down. The whole country is down.

He knows something is wrong. He just doesn’t know what.

So he does what Danish professionals do: he waits for someone to explain it.

But no one will.

Because the people who could explain it—the hedge funds with their filings, the analysts with their models, the administrators with their procedures—they don’t explain.

They extract.

And when they’re done extracting, they move on.

Leaving Lars with his red screen, his damaged pension, and a vague sense that something has been taken from him.

Something has.

Denmark stopped thinking a long time ago. It just didn’t notice until the screen turned red.

If this resonated, subscribe. The next installment—”The Hedge Fund Files”—will name the funds, trace the filings, and document exactly how sophisticated capital positioned for Denmark’s collapse while Danish institutions were busy writing articles about a Romanian CEO.

The extraction is documented. The pattern is visible. The choice is Denmark’s.

#realDenmark #The700BillionShort #SellGreenland #ShapeRobotics #TænkIgen