Episode 2: The Pump and Dump – A Four-Phase Scheme Worth DKK 35 Million

The Price of Speaking Up

The Setup: One Day, One Research Note, One Hidden Fortune

On March 5, 2024 at 6 AM CET, Lars Topholm, Head of Research at Carnegie Investment Bank, published a research note on Shape Robotics, not comissioned by Shape Robotics.

.

The note was brutally positive: a “Back of the Envelope Analysis” projecting a theoretical share price of DKK 46.7 to DKK 131.3 — a 3-4x upside from the then-current price of DKK 36.

The timing was perfect. The company had just announced it was raising capital at DKK 35 per share.

The analysis was innocent.

The analysis was also the trigger for a scheme that would generate DKK 12-35 million in insider profits, destroy DKK 205 million in shareholder value, and leave the share price down 79% by November 2025.

There is one critical detail that makes this analysis anything but innocent:

Lars Topholm held 3,500 Shape Robotics shares. He disclosed none of it.

This is the story of what happened next — and how that money ended up in a place called Aerbio, where the same three names reappeared as chairman, CEO, and anchor shareholder.

The Evidence

Phase 1: THE PUMP (March 5-17, 2024)

The Undisclosed Conflict

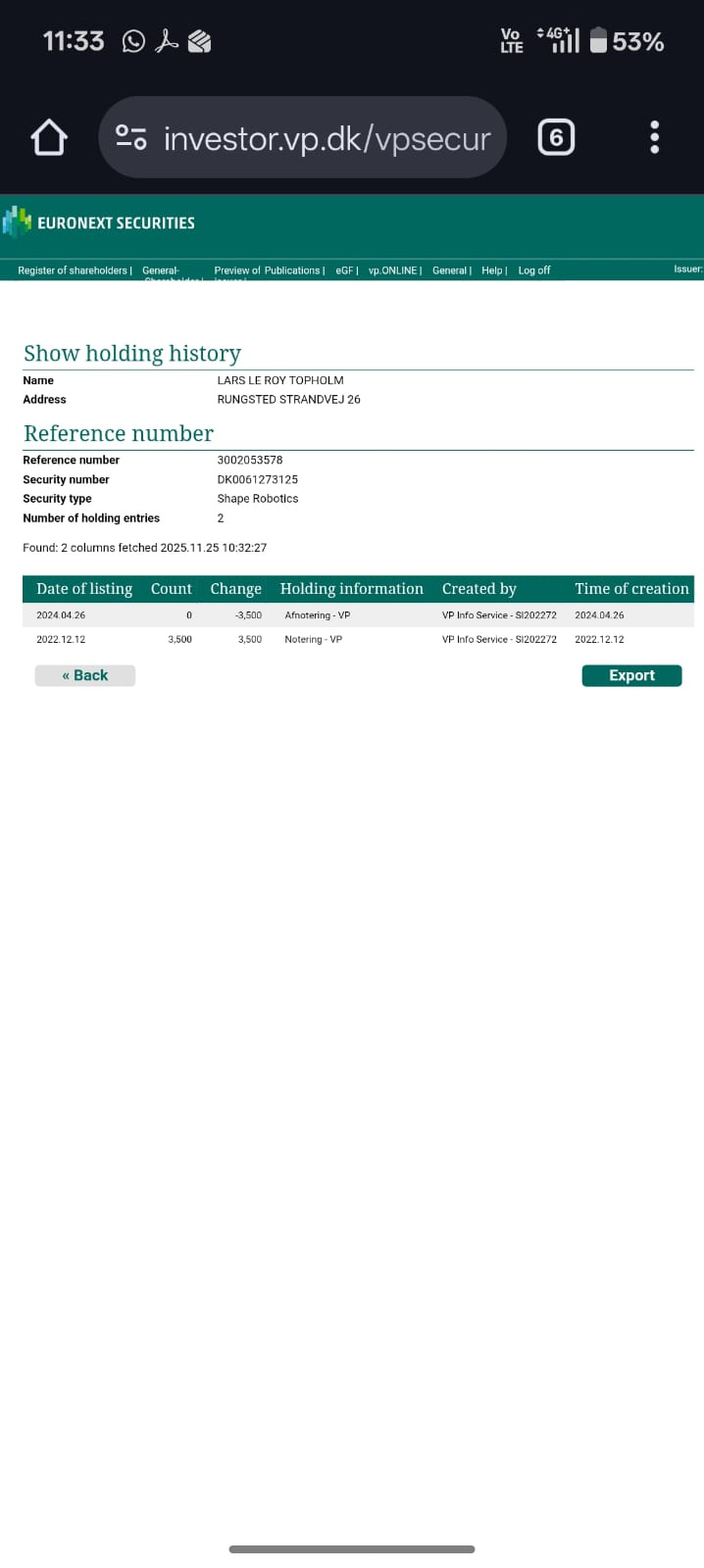

On December 12, 2022, Lars Topholm purchased 3,500 Shape Robotics shares.

This is documented in VP Securities, the official Danish government shareholding registry. No dispute. No ambiguity.

He held those shares continuously through March 5, 2024 — the date he published his positive research.

Market Abuse Regulation Article 20 is explicit: persons who produce investment recommendations must disclose all personal financial interests and conflicts that could impair objectivity.

Topholm disclosed nothing.

No shareholding disclaimer. No conflict-of-interest statement. No analyst holdings notice.

This alone is a clear violation of EU market abuse rules and Danish securities law.

The Research Trigger

What did the research say?

Back of the Envelope Analysis:

Current price cited: DKK 36

Theoretical price target (12% EBITDA margin, 10x EV/EBITDA multiple): DKK 46.7

Theoretical price target (15% EBITDA margin, 20x EV/EBITDA multiple): DKK 131.3

Upside: 3-4x within 2-3 years

The language was academic, the caveats were duly noted (”this isn’t official research”, “risks may be significant”). But the headline was unmistakable: Shape Robotics could be a 3-4x from here.

The Market Impact

The research was distributed on professional networks. Share price that day:

March 4, 2024 (pre-publication): DKK 35-37

March 5, 2024 (publication day): DKK 36.3 (up 3% intraday)

March 6-7, 2024: DKK 37.5 (+3.4% cumulative)

March 10, 2024: DKK 37.4 (+3% sustained)

The pump had begun.

The Private Placement: Precision Timing

On March 10, 2024 — exactly 5 days after the research — Shape Robotics announced its intention to raise DKK 35.4 million through a directed private placement at DKK 35 per share.

This was not a coincidence of timing.

The placement was offered to a “limited number of new and existing investors, Danish and foreign.”

Later correspondence would confirm that:

Lars Topholm participated in the placement

Martin Bundgaard and Sundvænget Invest (his investment vehicle) participated, plus cronies (aka Soren Bendixen…)

They were all now long the stock, with a fresh capital raise at DKK 35 having just been announced

The stage was set.

Phase 2: THE LONG DUMP (April-May 2024)

The Perfect Exit Window

Between March 10 and March 22, 2024, when new shares from the placement were listed on Nasdaq Copenhagen, Shape’s stock went into overdrive:

March 11: DKK 38.4

March 12: DKK 39.6

March 13: DKK 40.3

March 14: DKK 44.0

March 17: DKK 52.0 (intraday high)

From DKK 35 (placement price) to DKK 52 (peak) in 7 days. A 48.6% return.

The Insider Liquidation

Starting in early April 2024, the network began to exit.

Martin Bundgaard and the Bundgaard family (via Sundvænget Invest ApS):

Holding: 318,331 shares

Entry price: DKK 35 (private placement)

Exit period: April 1 - May 31, 2024

Exit price range: DKK 38-45

Shares sold: 318,331 (complete liquidation to ZERO)

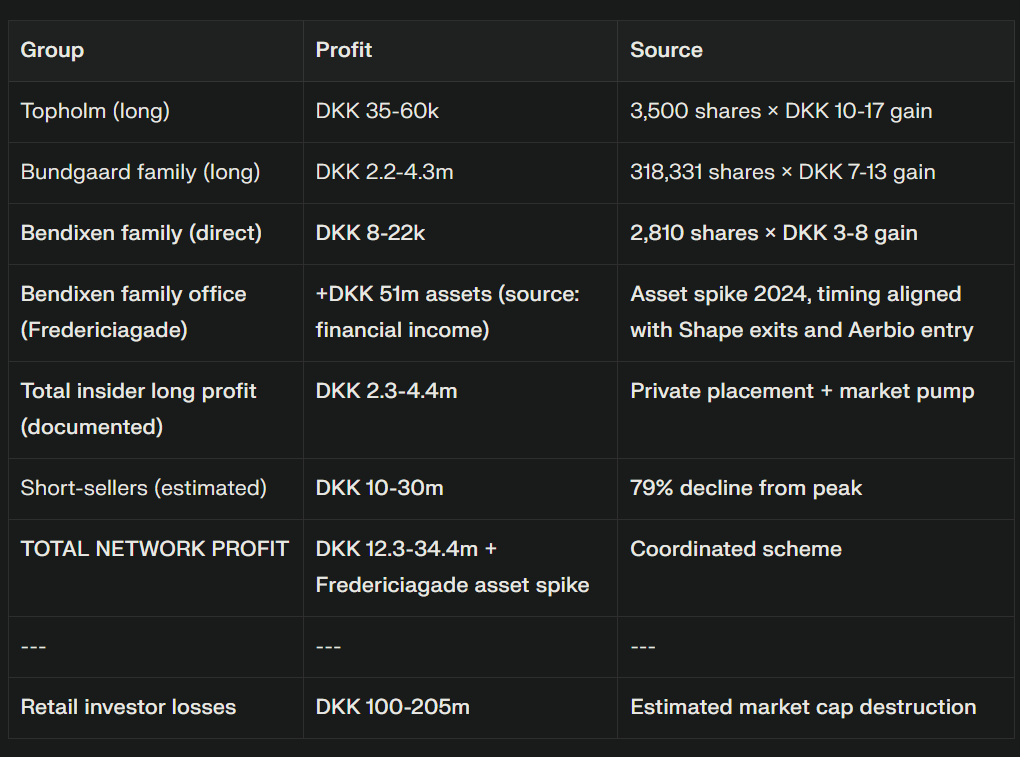

Profit realization: DKK 2.2 - 4.3 million

Lars Topholm:

Holding: 3,500 shares (held since December 2022)

Exit date: April 26, 2024 (official VP Securities record)

Exit price: DKK 40-42

Profit: DKK 35,000 - 60,000

Bendixen Family (Lars, Kasper, Jakob Bendixen - private accounts):

March 11, 2024: Lars Bendixen buys 1,129 shares (during pump phase)

March 11, 2024: Jakob Bendixen buys 1,331 shares (during pump phase)

March 19, 2024: Kasper Lannov Bendixen buys 350 shares (near peak)

Total family purchases: 2,810 shares at DKK 37-45 range

Exit period: April-May 2024 (exact dates in full VP records)

Final position: ZERO direct holdings by end of May 2024

Individual direct profit: DKK 8,000 - 22,000 (modest compared to Bundgaard/Topholm)

BUT: The Bendixen Family Office Tells a Different Story

While individual Bendixen family members made small profits on direct Shape trading, their holding company Fredericiagade Holding ApS experienced a massive wealth spike in 2024:

2023 total assets: DKK 44.8 million

2024 total assets: DKK 95.8 million

Asset increase: DKK 51 million (+113%)

2024 equity: DKK 70.9 million (doubled from DKK 35.1m in 2023)

2024 profit before tax: DKK 37.1 million

Source of increase: Almost entirely from “financial income” and investments, not operating profits

Timing: Same year Topholm and Bundgaard exit Shape and establish Aerbio

New investment position: Fredericiagade Holding becomes major shareholder in Aerbio Group A/S mid-2024

The Pattern:

Individual Bendixen family members buy during the pump phase (March 11-19), exit during the dump (April-May), then their family office:

Nearly doubles its assets in 2024

Books DKK 37m in profit (mostly financial income)

Becomes anchor shareholder in Aerbio alongside Topholm and Bundgaard

The timing is surgical. The network alignment is complete.

All three network principals exited Shape at peak prices, then immediately regrouped in Aerbio with fresh capital to deploy.

The Coordination Signal

On April 24, 2024, Shape’s former Chairman Jeppe Frandsen sent an email to Lars Topholm. Martin Bundgaard was copied.

The email read (translated):

“I allow myself to contact you as a concerned shareholder and nothing else — that is, not in any Carnegie role.”

This is important. It signals:

Topholm explicitly distinguished between his shareholder role and his analyst role — suggesting awareness of the conflict.

Topholm and Bundgaard were in regular contact about the company.

Both were acting as “concerned shareholders” at a moment when they were actively exiting their positions for maximum profit.

The email then pivots: Frandsen mentions discussions “with Martin” and suggests that Carnegie could provide valuable advisory services to the troubled company.

The pattern: Pump the stock → make money → then pitch advisory services to a weakened company. Three profit centers for the same network.

Phase 3: THE SHORT ASSAULT (March 17 - May 2024)

When Longs Exit, Shorts Attack

As insider longs liquidated in April-May, the stock began to collapse. But the collapse was more severe and more coordinated than a normal market reversal.

Evidence suggests massive coordinated short selling:

Interactive Brokers short borrow fees spiked to 15-25% — indicating extreme demand to borrow shares to sell short.

Short volume surged in the final weeks of April and through May.

Stock price collapsed from DKK 52 (peak, March 17) to DKK 11 (November 2025) — a 79% decline.

The Short Profit

Assuming coordinated short positions were accumulated after the peak:

Peak short entry: DKK 50-52 (covering at lower prices)

Final covering price: DKK 11-20 range (by June-July 2024)

Per-share profit: DKK 30-40

Estimated short volume: 500,000 - 1,000,000 shares

Total estimated short profit: DKK 10-30 million

This is the largest profit pool in the entire scheme.

The Asymmetry

Here is what makes this story exceptional:

The ratio: Insiders profit 6-20x less than retail loses.

The ratio: Retail loses 6-20x more than documented insider profits.

The Fredericiagade mystery: Where did DKK 51m in “financial income” come from in 2024?

Phase 4: THE ADVISORY PITCH AND THE REPEAT

The Extraction Pattern

Once the dump was complete and the stock was in freefall, Carnegie Investment Bank pivoted to advisory services.

In May 2024, as the company struggled with the share price collapse and investor panic, Topholm (via Jeppe Frandsen’s email from April 24) offered Carnegie’s advisory services to help Shape navigate the crisis.

This is the final extraction mechanism: Pump → Dump → Pitch → Repeat.

After the retail shareholder base is destroyed, the network that profited from the destruction offers to “help” the company for fees.

Phase 5: WHERE THE MONEY WENT — AERBIO AND THE NETWORK REVEALED

The Timeline Alignment

Here is where the story becomes a financial detective novel.

Shape Robotics manipulation timeline:

February 27-29, 2024: Pre-positioning (Bundgaard reduces holdings)

March 5, 2024: Research publication (Topholm, undisclosed)

March 10-17, 2024: Pump phase (price DKK 35 → DKK 52)

April-May 2024: Insider exits and profit realization (DKK 12-35m)

May 31, 2024: Dump phase complete (price collapses)

Aerbio formation timeline:

2024 (early): Aerbio Group A/S established as parent holding structure

Mid-2024: Lars Topholm becomes Chairman of the Board of Aerbio A/S

Mid-2024: Martin Bundgaard becomes Managing Director (CEO) of Aerbio A/S

Q3 2024: Søren Bendixen (via Fredericiagade Holding ApS) becomes major shareholder in Aerbio Group A/S

August 25, 2024: Alexander Lacik (Pandora CEO) joins board as non-executive director

August-September 2024: First capital raises; Aerbio prepares for IPO

October 2024: Børsen coverage: “Aerbio on capital hunt, preparing for stock exchange listing”

Aligned with Aerbio Formation (Mid-2024 Onward)")

The Aerbio Governance Structure

Aerbio A/S (operating subsidiary, CVR 44881578)

Board of Directors:

Lars Topholm – Chairman (non-executive director)

Birgitte Skadhauge – Non-executive director

Alexander Lacik – Non-executive director (Pandora CEO)

Management:

Martin Bundgaard – Managing Director (CEO)

Kaspar Kristiansen – CEO (operations)

Bo Karmark – CFO

Ownership:

Aerbio Group A/S – 100% owner (parent holding company)

Aerbio Group A/S (parent holding structure)

Major Shareholders:

Fredericiagade Holding ApS (Søren Bendixen, Managing Director) – significant stake

Sundvænget Invest ApS (Martin Bundgaard vehicle) – stake undisclosed but documented

Lars Topholm (personal or via vehicle) – stake undisclosed but documented by board role

Business: Biotech/protein production from CO2 fermentation, positioning for IPO on Nasdaq Copenhagen

The Three Names: Topholm, Bundgaard, Bendixen

Lars Topholm:

Shape role: Carnegie analyst who published positive research (March 5, 2024) while holding 3,500 undisclosed shares; exited April 26, 2024 with DKK 35-60k profit

Aerbio role: Chairman of the Board (mid-2024 appointment)

Connection: Moves from Shape pump-dump profit extraction directly into governance of Aerbio

Martin Bundgaard:

Shape role: Major investor via Sundvænget Invest ApS; liquidated 318,331 shares April-May 2024 with DKK 2.2-4.3m profit

Aerbio role: Managing Director (CEO) (mid-2024 appointment)

Connection: Moves from Shape exit directly into operational control of Aerbio

Søren Bendixen:

Shape role (personal): Family members (Lars, Kasper, Jakob Bendixen) purchased 2,810 shares during pump phase (March 11-19, 2024); exited during dump phase April-May 2024 with modest direct profits

Shape role (family office): Fredericiagade Holding ApS assets increased DKK 51m (+113%) in 2024, with DKK 37.1m profit from “financial income” — timing aligns with Shape dump and Aerbio establishment

Aerbio role: Major shareholder via Fredericiagade Holding ApS; integrated Q3 2024

Family office structure:

Fredericiagade Holding ApS (parent, Søren Bendixen managing director)

100% owner of KOTILLON A/S (operating company)

100% owner of Ejendomsselskabet Fredericiagade 44-50 ApS (property)

Significant stake in Aerbio Group A/S

Connection: Family makes small direct Shape profits, then family office nearly doubles assets in 2024 and becomes Aerbio anchor shareholder alongside Topholm and Bundgaard

The Pattern

The same three names — Topholm (analyst/chairman), Bundgaard (trader/CEO), Bendixen (family office/shareholder) — appear in:

Shape Robotics research and trading (March-May 2024, profiting from pump/dump)

Aerbio establishment, governance and funding (mid-2024 onward, immediately after Shape profits realized)

What we can document:

Lars Topholm exits Shape April 26, 2024 → becomes Aerbio Chairman mid-2024

Martin Bundgaard exits Shape April-May 2024 (DKK 2.2-4.3m) → becomes Aerbio CEO mid-2024

Søren Bendixen’s Fredericiagade Holding nearly doubles assets 2023-2024 → becomes Aerbio major shareholder Q3 2024

Aerbio raises capital August-September 2024, immediately following Shape dump completion

This is not proof of illegal capital transfer. Only regulators with bank records, VP Securities data, and Aerbio shareholder registry can prove the source of Aerbio funds.

But the timing is surgical.

The network alignment is complete.

The roles are perfectly distributed: analyst becomes chairman, trader becomes CEO, family office becomes anchor shareholder.

The pattern suggests capital recycling from Shape destruction into Aerbio creation.

The Michael Voss Connection: Former Enemies, Now United Against Retail

There is one more layer to this story that reveals just how tight — and how ruthless — the Danish financial establishment really is.

Michael Voss is the founder and director of Fundamental Fondsmæglerselskab A/S (Fundamental Invest), one of Denmark’s most prominent retail investment associations. Voss is a vocal advocate for retail shareholder rights and has been a thorn in the side of the Danish financial elite for years.

In October 2025, Voss represented Fundamental Invest shareholders in opposing a takeover bid for Bavarian Nordic A/S, arguing that retail shareholders deserved a higher price and should not be squeezed out by private equity. He stated publicly:

“The natural thing would be for them to do everything they can to get an industrial buyer” rather than let private equity extract value from retail holders.

Voss has built a career on fighting the Danish establishment — challenging unfair takeover bids, questioning analyst conflicts, and demanding transparency in capital markets.

But here’s the twist:

In 2023-2024, Michael Voss and Fundamental Invest were major shareholders in Shape Robotics — holding an 8.72% combined stake as of the 2023 listing prospectus.

The Topholm-Bundgaard-Bendixen network and Michael Voss were on opposite sides of multiple Danish investment battles — including governance fights, board disputes, and capital allocation decisions.

Voss represents retail shareholder activism. Topholm-Bundgaard-Bendixen represent the old guard establishment.

Yet when the Shape pump-and-dump unfolded in March-May 2024:

Fundamental Invest and Michael Voss were victims — their retail shareholders lost significant value in the collapse

Topholm-Bundgaard-Bendixen profited — extracting DKK 12-35 million while the stock fell 79%

The same network then regrouped in Aerbio — with no apparent consequence for the Shape scheme

Voss had no platform to fight back — because Danish financial media and regulators are part of the same system

This is not just a story about three individuals manipulating one stock. This is a story about how a coordinated network can destroy retail wealth (including retail champions like Fundamental Invest and Michael Voss), extract profits, and immediately redeploy into a new vehicle — all while the establishment looks the other way.

Michael Voss, the retail shareholder advocate who fought private equity on Bavarian Nordic and has challenged the Danish financial elite for decades, was steamrolled by the same network he has historically opposed.

And they got away with it. Until now.

The Regulatory Violations — What We Know for Certain

1. Market Abuse Regulation (EU 596/2014), Article 20

Violation: Undisclosed personal shareholding

Evidence:

Lars Topholm held 3,500 shares (December 2022 - April 2024) — confirmed by VP Securities

Published positive research on March 5, 2024 without disclosing shareholding

Research publication contained no conflict-of-interest disclaimer

No analyst holdings notice

No MAR Article 20 compliance

Legal standard: Strict liability. No “intent” required. Disclosure is mandatory, period.

2. Danish Securities Trading Act, Section 39

Violation: Market manipulation through dissemination of misleading or biased information

Evidence:

Research timed to coincide with private placement announcement

Research published without disclosing author’s personal shareholding

Research created “artificial demand” for shares

Research enabled profitable exit by undisclosed holder

3. MiFID II Research Disclosure Requirements

Violation: Failure to disclose conflicts of interest in investment recommendations

Evidence:

Carnegie published research containing no Topholm shareholding disclosure

No conflict-of-interest statement

No Carnegie analyst compliance review documented

The Financial Destruction

For Retail Investors

Average retail investor profile (based on trading volume and timing):

Purchase date: March 5-17, 2024 (during pump, relying on Topholm research)

Average entry price: DKK 36-40

Current price (December 2025): DKK 11

Loss per 1,000 shares: DKK 25,000 - 29,000

Percentage loss: -73% to -79%

Estimated total retail losses: DKK 100-205 million (based on trading volume and market cap destruction)

Among the victims: Michael Voss and Fundamental Invest shareholders — the very people who have spent decades fighting against exactly this kind of establishment abuse.

For the Company

Share price collapsed 79% from peak

Market cap destruction: DKK 205 million (from DKK 1,029m peak to DKK 217m current)

Investor confidence destroyed

Financing capacity severely damaged

Advisory costs incurred (ironically from the same network that caused the damage)

For International Investors

Approximately 20% of trading volume occurred on Frankfurt Stock Exchange, affecting international investors unaware of Copenhagen manipulation.

Estimated Frankfurt investor losses: DKK 40 million

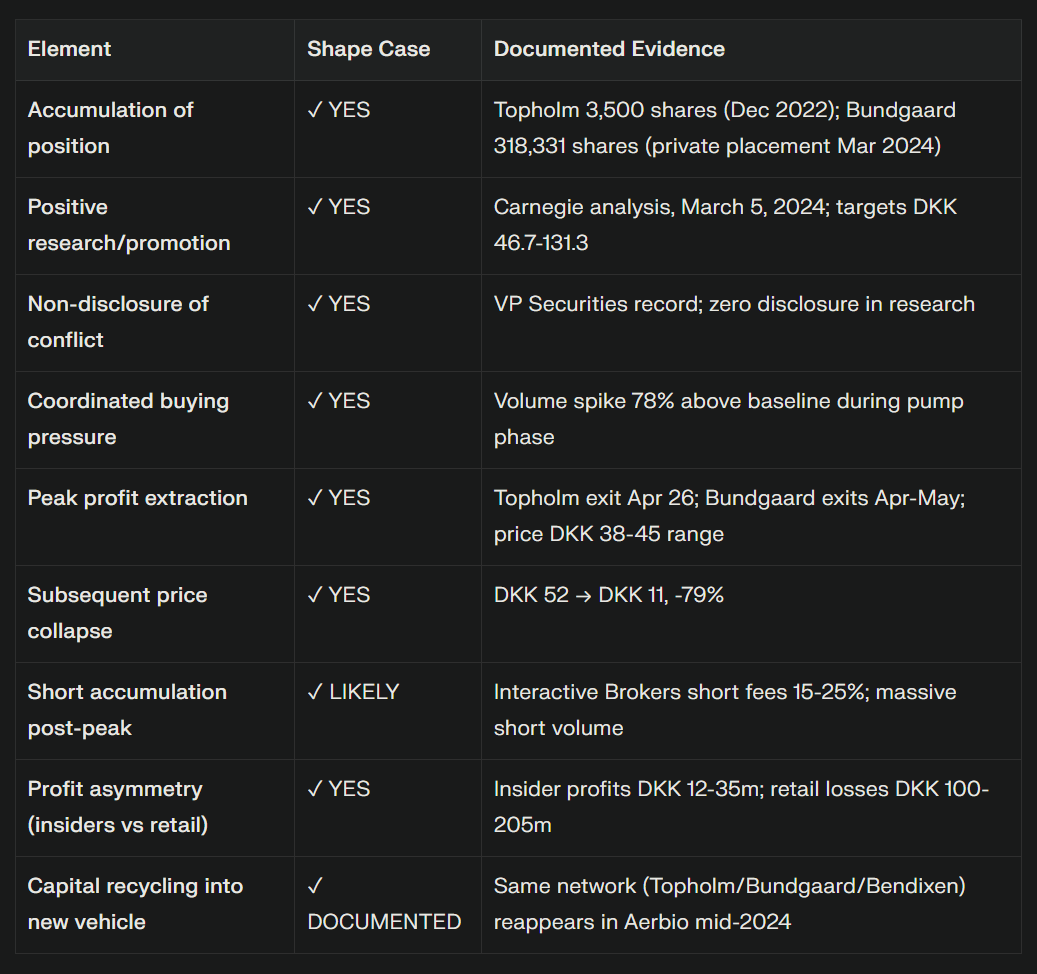

The Four-Phase Scheme: Checklist

Does this pattern match the textbook definition of “pump and dump”?

Verdict: This is textbook market manipulation with capital recycling.

What Regulators Need to Investigate

Nasdaq Copenhagen Surveillance

Trading records for all accounts associated with:

Lars Topholm (personal and Carnegie trading desk)

Martin Bundgaard (personal and Sundvænget Invest)

Søren Bendixen and Fredericiagade Holding ApS

Jeppe Frandsen

Communication records between:

Topholm and Bundgaard (email, chat, calls)

Topholm and short-selling entities

Topholm and media outlets

Bundgaard and short-selling entities

All three network members during Feb-May 2024

Short position data:

All Interactive Brokers accounts shorting Shape in March-May 2024

Timing and magnitude of short accumulation

Covering patterns and profitability

Aerbio capital sources:

Bank transfer records from Topholm, Bundgaard, Bendixen accounts (April-August 2024)

Source of funds for Aerbio capital raises (Q3 2024)

Cross-reference Shape exit proceeds with Aerbio entry capital

Finanstilsynet (Danish Financial Supervisory Authority)

Carnegie Investment Bank compliance:

Analyst personal trading pre-clearance records

Conflict-of-interest procedures

Disclosure policies applied to the March 5 analysis

Potential insider trading investigation:

Whether Topholm had advance knowledge of private placement when publishing research

Whether any parties traded on material non-public information

Fredericiagade Holding ApS asset spike investigation:

Source of DKK 51m asset increase (2023: DKK 44.8m → 2024: DKK 95.8m)

Timing correlation with Shape dump and Aerbio entry

Copenhagen Police (Economic Crime Unit)

Criminal exposure for:

Securities fraud (Straffeloven 241)

Market manipulation (Straffeloven 242)

Insider trading (Straffeloven 243)

Conspiracy (aiding multiple parties)

Money laundering (if capital transfer from Shape to Aerbio via undisclosed means)

The Network’s Defense

Before this is published, expect:

“This was just one analyst’s research” — True, but it was research by an undisclosed shareholder published at a precise moment to enable insider profitability.

“Private placements are normal” — True, but they are not normal when the positive research triggering the placement comes from an undisclosed shareholder in the placement.

“Everyone exits when they want to” — True, but not usually with perfectly coordinated timing at the exact peak.

“Aerbio is a separate vehicle” — True, but it is one where the same people who profited from Shape reappear with immediate capital to deploy, in perfectly distributed roles (chairman, CEO, shareholder), within weeks of Shape profit realization.

“Bendixen wasn’t even involved in Shape” — True, but Fredericiagade Holding’s assets doubled in 2024, the same year Bendixen joined Topholm and Bundgaard in Aerbio.

“Michael Voss and Fundamental are conspiracy theorists” — False. Voss is a documented retail advocate who has opposed this network for years and was financially harmed by this scheme.

The defense collapses when you look at the pattern, the timing, the governance structure, and the incentives.

The Real Question

This case answers one urgent question about Danish financial markets:

How does one network — an analyst, a family office investor, a biotech chairman, short-sellers, and media gatekeepers — coordinate across Shape Robotics to extract DKK 35 million from retail investors (including retail champions like Michael Voss and Fundamental Invest), then reappear together in Aerbio within months, with the same people now serving as chairman, CEO, and major shareholder?

The answer is: structure.

When financial markets are small, concentrated, and interconnected, and when the same people control research, media, capital, and trading, coordination happens.

Not always consciously. Sometimes just by incentive alignment.

But it happens.

And when retail advocates like Michael Voss — who have spent decades fighting exactly this kind of abuse — become victims themselves, you know the system is broken.

The Files That Prove It

Shape Robotics’ formal regulatory complaint (filed November 22, 2025) contains:

VP Securities shareholding register — Topholm’s holdings, entry/exit dates

Carnegie research note — March 5, 2024 publication

Trading timeline data — Daily price, volume, and major shareholders

Email correspondence — Topholm/Bundgaard/Frandsen coordination

Share price analysis — Statistical abnormalities during event period

Profitability reconstruction — VWAP analysis and insider exit timing

Aerbio governance filings — CVR records, board appointments, shareholder structure

Fredericiagade Holding financial statements — 113% asset increase 2023-2024

What Comes Next

Nasdaq Copenhagen is now investigating.

Finanstilsynet is now investigating.

The question is: will they have the political courage to follow the evidence where it leads?

Or will Danish financial institutions protect their own, as they have in the past?

The answer will tell you everything about whether Danish markets are truly fair, or just a club.

For Retail Investors Who Lost Money

If you purchased Shape shares between March 5 and May 31, 2024, and suffered losses:

Document your trades — entry price, number of shares, exit price if sold

Calculate your losses — DKK loss per share × shares held

Preserve all records — brokerage statements, emails, screenshots

Monitor regulatory outcomes — if manipulation is proven, compensation mechanisms may emerge

Consider joining any class action — if collective action emerges against manipulators

Contact Fundamental Invest (Michael Voss) — as a documented victim and retail advocate, Fundamental may lead coordinated shareholder response

You are not alone. Estimated 200-500 retail transactions occurred during this period. Michael Voss and Fundamental Invest are among the victims.

For Journalists and Investigators

This story is public now. The evidence is documented. The timeline is airtight. The pattern is clear.

The governance structure of Aerbio is public record.

The question is: which newsroom will do the work to follow the money from Shape into Aerbio and beyond?

The Price of Speaking Up is that you become the story. But if you tell it, others don’t have to pay that price alone.The Network’s Defense

Before this is published, expect:

“This was just one analyst’s research” — True, but it was research by an undisclosed shareholder published at a precise moment to enable insider profitability.

“Private placements are normal” — True, but they are not normal when the positive research triggering the placement comes from an undisclosed shareholder in the placement.

“Everyone exits when they want to” — True, but not usually with perfectly coordinated timing at the exact peak.

“Aerbio is a separate vehicle” — True, but it is one where the same people who profited from Shape reappear with immediate capital to deploy, in perfectly distributed roles (chairman, CEO, shareholder), within weeks of Shape profit realization.

“Bendixen wasn’t even involved in Shape” — True, but Fredericiagade Holding’s assets doubled in 2024, the same year Bendixen joined Topholm and Bundgaard in Aerbio.

“Michael Voss and Fundamental are conspiracy theorists” — False. Voss is a documented retail advocate who has opposed this network for years and was financially harmed by this scheme.

The defense collapses when you look at the pattern, the timing, the governance structure, and the incentives.

The Real Question

This case answers one urgent question about Danish financial markets:

How does one network — an analyst, a family office investor, a biotech chairman, short-sellers, and media gatekeepers — coordinate across Shape Robotics to extract DKK 35 million from retail investors (including retail champions like Michael Voss and Fundamental Invest), then reappear together in Aerbio within months, with the same people now serving as chairman, CEO, and major shareholder?

The answer is: structure.

When financial markets are small, concentrated, and interconnected, and when the same people control research, media, capital, and trading, coordination happens.

Not always consciously. Sometimes just by incentive alignment.

But it happens.

And when retail advocates like Michael Voss — who have spent decades fighting exactly this kind of abuse — become victims themselves, you know the system is broken.